05 Mar Our rate recommendation? Go variable.

The most common question we receive is, “Should I go fixed or variable?” While we don’t have a crystal ball, there are certain trends we have come to notice from closely watching rate changes over the last decade. Ultimately, fixed and variable rates are impacted by outside economic factors. Not always, but generally, when the economy is flourishing, rates increase. When the economy is slowing or in recession, rates will drop. The government wants to encourage spending by decreasing rates during recession.

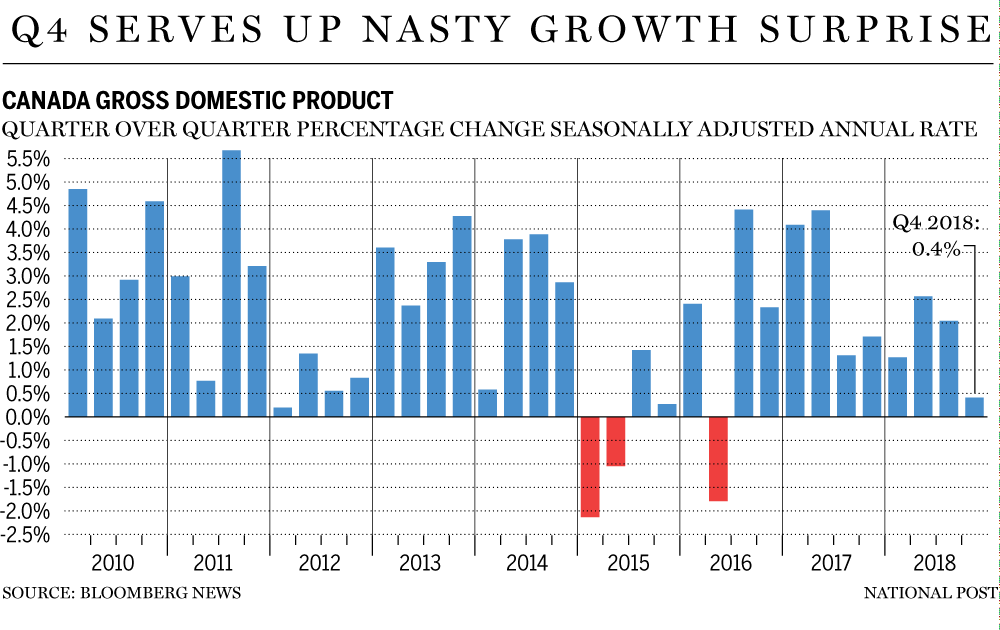

If you have followed rate hikes over the past 18 months, it would not be a surprise for borrowers to be uneasy when considering a variable rate. An adjustable rate is known synonymously with a variable rate mortgage. And, while they aren’t identical, for the purpose of this article, we’ll call them the same. In June 2017, Prime rate was 2.70%. Fast forward to 2019, and Prime is 3.95%. So, why do we recommend variable rate? Well, a recent report from Stats Canada, shows the economy in the 4th Quarter of 2018 came to a grinding halt. The numbers were flat out bad. It was the worst 4th quarter performance in two and a half years! Check out the link below for more information:

Many borrowers who chose a fixed rate between 2015-2017, have an interest rate with a few years left between 2.39%-2.99%. In this case, we wouldn’t recommend touching your fixed rate. However, if your rate has more than a few years left and is over 3.50%, it might be worth the consideration. There are some products available as low as Prime minus 1.00% which would bring a current rate under 3%. If Canada heads into a recession, as the indicators suggest, the discount of 1% of prime could very helpful in a few years.